A week ago, we described the SmarTech Analysis report, which described the current situation in the 3D printing industry in the world. The conclusions from the report were very optimistic – the value of the additive technology market is growing and these are two-digit values only compared to the previous year. This week, another analytical company, CONTEXT, published its report, presenting more detailed data on individual market sectors. The general conclusion is the same – the 3D printing market is growing dynamically, but mainly in the area of industrial systems. The market of cheap, amateur 3D printers has slowed down significantly…

As in the case of the SmarTech report, the CONTEXT study pays attention to the change in the direction of development of the broadly understood manufacturing sector, where, due to the deepening problems with the continuity of supply chains, the so-called production on demand. Of course, this process has only just begun and it will be many years before this paradigm becomes dominant, but at this early stage it is significantly reflected in the increase in sales of industrial – production 3D printers.

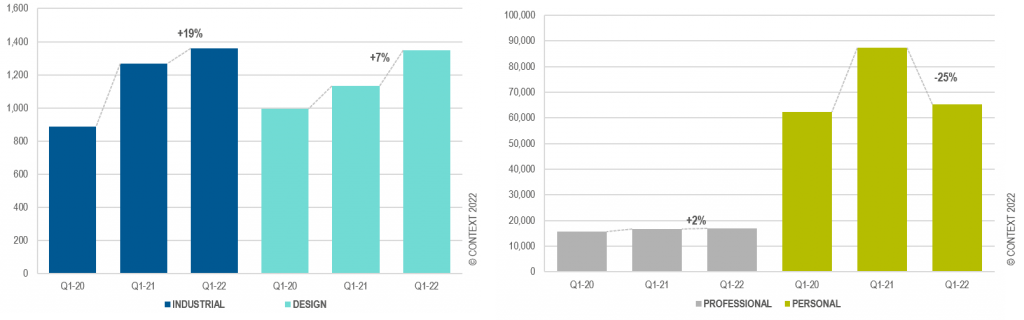

In Q1 2022, devices classified as “industrial” (3D printers for metal, powdered plastics or high-performance plastics in the form of filament) and “design” (3D printers for resins or smaller filament systems) recorded sales increases of +7% respectively and + 19% compared to the first quarter of the previous year. In total, revenues from the sale of these machines accounted for 69% of the total revenues of the 3D printing industry in the first quarter of this year. This increase is even more impressive compared to the same period in 2020, just before the pandemic – industrial system deliveries increased by +53% and design systems increased by +36%.

On the other hand, sales of “consumer” and amateur (DIY) 3D printers decreased by -25% and -47% respectively compared to the first quarter of 2021. Sales of desktop-class 3D printers, which constitute the intermediate segment, were relatively stable: only +2 % year on year and +7% compared to Q1 2020.

As for industrial machines, the largest increase was recorded in the case of 3D printing devices from powdered metals in the Binder Jetting technology, where deliveries increased by + 113% compared to the first quarter of 2021. At the same time, CONTEXT emphasizes that the Binder Jetting method is not the dominant technology and accounts for only 3% of all supplies of industrial machines, and is also not dominant in the area of 3D metal printing alone, accounting for only 8% of the total category. Of course, the greatest merit in this field is due to Desktop Metal and the ExOne acquired last year, although CONTEXT expects that this situation may soon change when the long-announced HP metal 3D printers are available for sale.

In terms of the total number of machine deliveries, the Chinese company UnionTech again took the lead in the ranking in terms of quantity, but recorded a decrease in deliveries of -6% compared to the previous year. The regions that currently lead the global growth in sales of industrial machinery are North America (+16% growth) and Western Europe (+ 8%). According to suppliers, the standout brands in the top ten that recorded the highest increases are Prodways, BMF, 3D Systems, Farsoon and HP in the segment of 3D printing with plastic powders, and Eplus3D, Velo3D, TRUMPF and Farsoon in the segment of 3D printing in metals.

In the design machinery segment, the leaders were HP with MultiJetFusion technology (+53% YoY increase) and Stratasys with PolyJet technology (+ 44% increase). In addition to these two, 3D Systems, Markforged, Nexa3D and Prodways have become the delivery leaders in this segment.

MakerBot and Ultimaker are the leaders when it comes to the desktop-class 3D printer sector, which recently announced a merger. Formlabs, Raise3D and SprintRay were the next companies on the list. At the same time, CONTEXT sees an increase in the share of 3D printer manufacturers in the education sector, citing Zortrax and its sales increases generated by the Laboratoria Przyszłości program as an example.

Source: www.contextworld.com

Photo: www.pixabay.com

{kind=link}